Area Agencies on Aging Services for Families

A Decentralized Network, Not a Single Agency There is no national Area Agency on Aging. That is the first thing worth getting straight, because the name implies a unified…

A Decentralized Network, Not a Single Agency

There is no national Area Agency on Aging. That is the first thing worth getting straight, because the name implies a unified institution, and the reality is something messier and more interesting: 618 separate agencies, each designated by its state to serve a defined geographic area, ranging from a single large city to a sprawling multi-county rural district. Some operate within county governments, roughly 31% according to USAging. About 23% function inside regional planning councils. The rest are scattered across configurations that reflect decades of local political negotiation more than any coherent design philosophy.

I have spent enough time inside this network to stop being surprised by how different two adjacent AAAs can feel. Call one and reach a case manager who has your situation mapped within fifteen minutes. Call another and navigate a phone tree to a voicemail. That variation is not dysfunction, exactly. It is what happens when you build a national system on a foundation of local governance and then tell local governance to figure out the rest.

The broader architecture places AAAs inside a structure authorized by the Older Americans Act: 56 state agencies on aging sit above them; nearly 20,000 local service providers and 281 Tribal organizations form the delivery layer beneath them. The Administration for Community Living funds and oversees the whole structure at the federal level. AAAs occupy the middle, and that position is consequential in ways that are not immediately obvious. They do not simply deliver services. They develop area plans based on local demographics and consumer input, coordinate networks of local providers, and function as the connective tissue between a federal policy written in Washington and the person who needs a ride to a nephrology appointment on Tuesday in a county where the nearest dialysis center is forty minutes away.

The practical implication for any family trying to use this system: the AAA is the first door to open, but what is behind it depends significantly on where you live. Decentralization produces local responsiveness. It also produces local inequity, and those two outcomes are inseparable.

The Range of What AAAs Actually Coordinate

Families managing a parent's declining health rarely need just one thing. They need a meal delivered, a ride arranged, a legal question answered, a Medicaid application navigated, and someone to call when the situation shifts at nine on a Friday night. The catalog of services AAAs coordinate is built around that reality, which is itself the point.

Core categories include information and referral, in-home care, home-delivered and congregate meals, adult day programs, case management, transportation, and legal assistance. The organizing principle across all of them is keeping independent living viable for people 60 and older. These services are not designed to manage institutional placement; they are designed to prevent or delay it. Every item in the catalog is, at some level, a bet that community support is both cheaper and better than institutional care. The evidence mostly supports that bet, though the evidence is stronger in some domains than others.

Aging and Disability Resource Centers, which function as a single point of entry within the broader network, are worth knowing by name specifically because many families never encounter them through the AAA's main line. They offer free, objective counseling across federal, state, and other programs. The word "objective" matters here more than it might seem: a benefits counselor at an ADRC has no financial stake in which program you enroll in, which is a rarer condition than it should be in the long-term care space.

Families and caregivers also receive services in their own right, not only on behalf of the person they are caring for. Long-term care planning consultations, typically free through the network, give families structured access to thinking they would otherwise purchase from an elder law attorney or piece together from sources of uneven reliability. Legal services, including free and reduced-rate help for both seniors and family members, round out the picture alongside referrals to the Long-Term Care Ombudsman for those navigating facility or home care settings.

The breadth here is not accidental. It reflects decades of program-level learning about what combination of supports actually keeps people out of nursing homes. Whether current funding is sufficient to deliver on that range is a separate and more uncomfortable question.

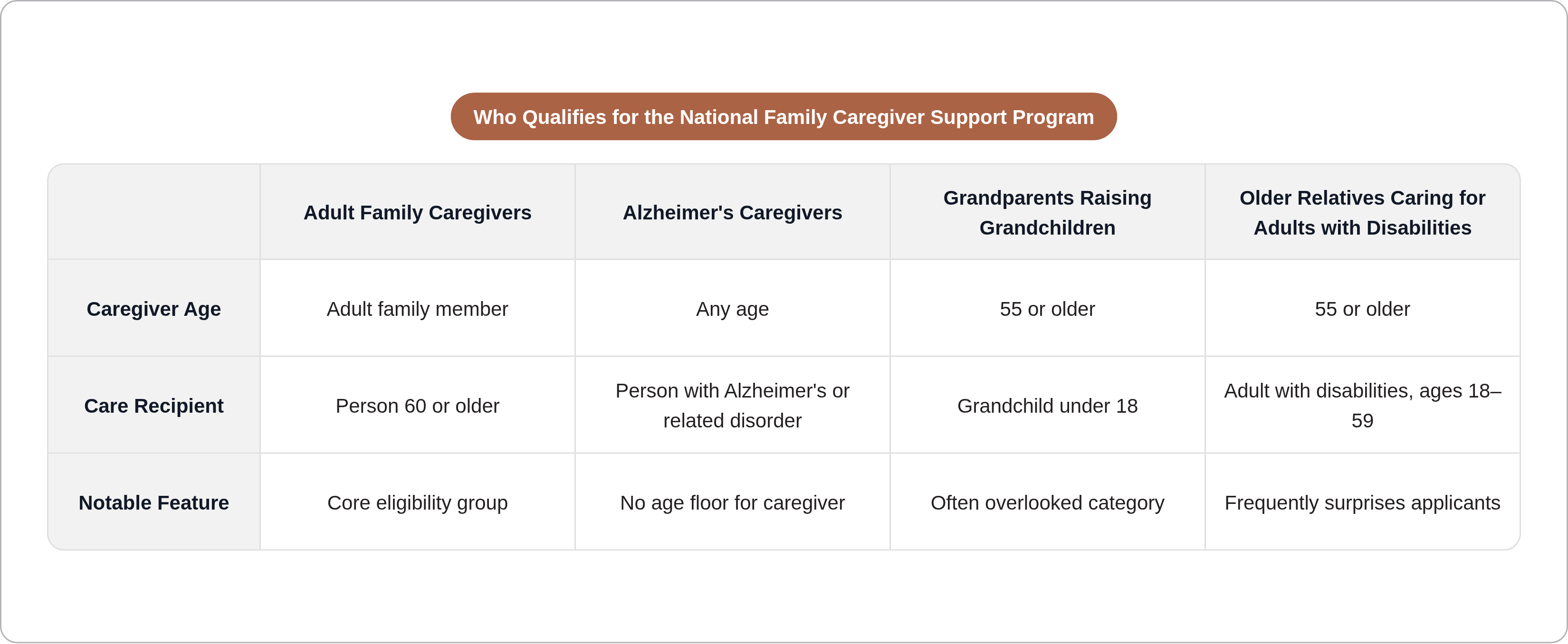

The National Family Caregiver Support Program: Built for the Person Doing the Work

The National Family Caregiver Support Program was established in 2000 and represented a genuine design departure from most aging-network services, which are organized around the care recipient. The NFCSP is organized around the caregiver. That distinction took years to earn policy legitimacy, and in many circles it still has not fully landed.

Eligibility is broader than most families assume. The program covers adult family members caring for someone 60 and older; caregivers of any age caring for someone with Alzheimer's disease or a related disorder; grandparents 55 and older raising grandchildren under 18; and older relatives 55 and older caring for an adult with disabilities between 18 and 59. That last category tends to catch people off guard when they first encounter it.

What caregivers can actually receive includes respite care, individual counseling, peer support groups, caregiver education and training, and emergency assistance. The respite component is where the clinical significance is most concentrated. According to ACL survey data, the program provided respite to more than 604,000 caregivers through nearly six million hours of relief. Seventy-four percent of caregivers of OAA program clients report that services enabled them to provide care longer than they otherwise could have. That is the program's clearest proof of concept.

A 2024 USAging survey of 616 AAAs found that 76% now have a caregiver program coordinator or manager on staff. The infrastructure exists at most agencies. That raises a question I keep coming back to: if the infrastructure is there, why do so many caregivers never access it? In most cases, the answer is that they did not know to ask, and nobody told them specifically enough that there was something to ask for.

The economic frame deserves explicit statement. Unpaid caregiving is valued at over $1 trillion annually in the United States. Without supportive services, nearly 62% of caregivers report the person they care for would otherwise be living in a nursing home. That is not a marginal finding. It describes a load-bearing function being performed, at scale, by individuals who are largely doing it without formal support and without the language to name what they need.

The Long-Term Care Ombudsman: A Formal Channel for Families Without One

Institutional settings strip older adults of the ordinary mechanisms for self-advocacy. Residents with cognitive impairment, physical dependence, or social isolation cannot reliably report substandard care, dispute a bill, or assert their legal rights without outside support. This is not a hypothetical concern. It is the operational reality that produced the Long-Term Care Ombudsman program.

Every state has an Office of the State Long-Term Care Ombudsman. Local programs are funded in part through the OAA and operate in all states, the District of Columbia, Puerto Rico, and Guam. In federal fiscal year 2023, over 1,500 full-time-equivalent staff and 3,443 trained volunteers worked the program. They handled 202,894 complaints and resolved or partially resolved 71% of them to the satisfaction of the resident or complainant. Sixty percent of all nursing homes were visited at least quarterly that year.

What ombudsmen actually do is investigate and resolve complaints, educate residents and families about residents' rights, and maintain a visible presence inside facilities. The visibility matters as much as the investigation function. A facility that expects quarterly visits operates under different conditions than one that does not, and anyone who has spent time inside long-term care settings knows that ambient accountability shapes behavior in ways that formal complaint processes alone do not.

For families, the Ombudsman program is a formal channel that many are unaware of, or unaware that it is accessible through their local AAA. It is particularly relevant during a parent's transition into a facility, when navigating a home care agency relationship, or when something feels wrong in a hospice situation and a family is uncertain what recourse looks like. The program does not guarantee resolution. It is a structural mechanism for power in settings where power is otherwise asymmetrical, and that framing is the right one.

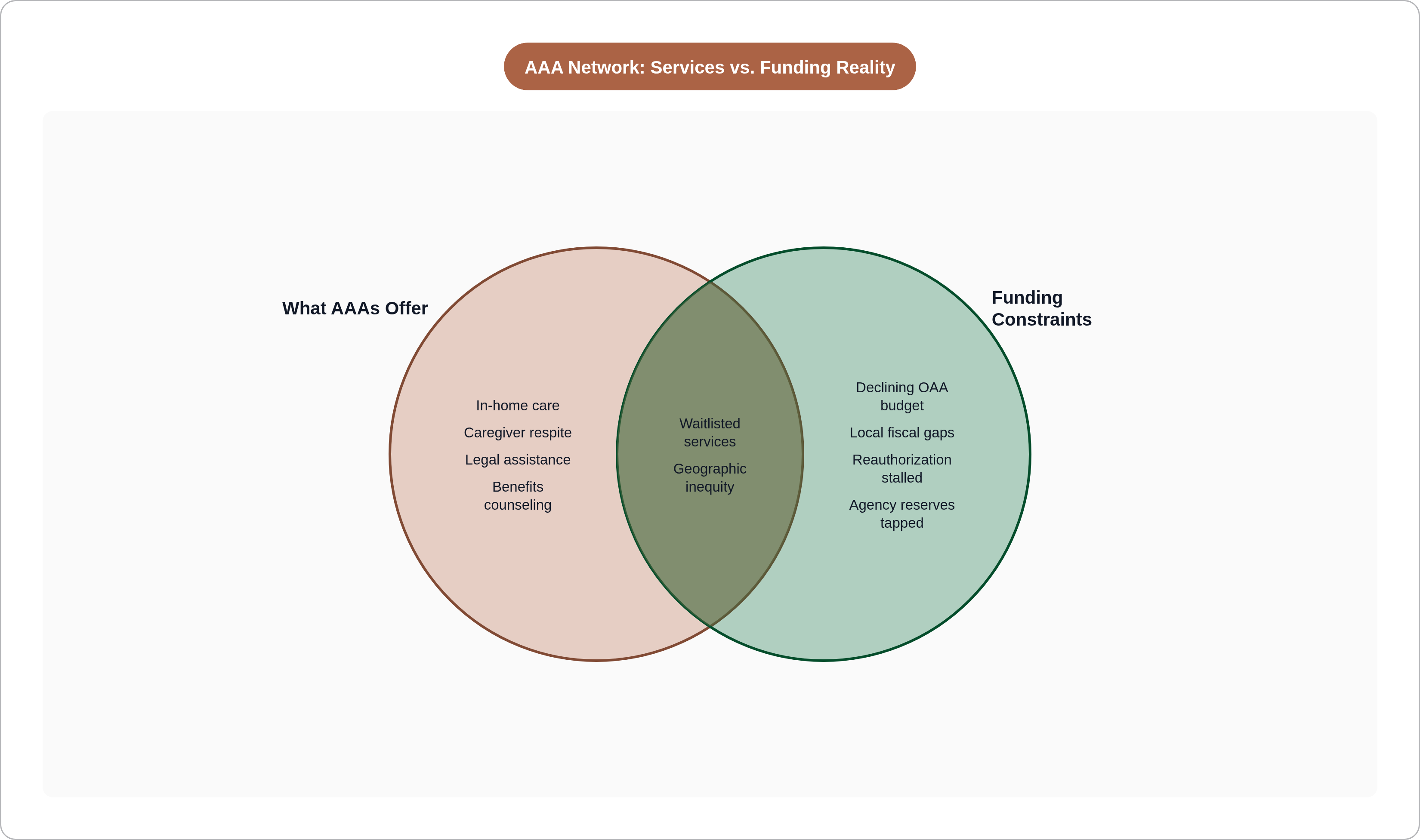

The Funding Gap: Structural, Not Incidental

Total OAA funding for fiscal year 2024 is $2.372 billion, a slight decline from the prior year. From 2012 to 2024, the median AAA budget grew 25% in inflation-adjusted terms. Over roughly the same period, the 65-and-older population grew 39%. The gap between resources and the population they are meant to serve has been widening for over a decade. It is not the result of neglect in any single budget cycle. Rather, it is structural divergence, compounding quietly.

Fifty-five percent of AAAs rely on local funding streams, including county revenues, to supplement federal dollars. Service availability tracks local fiscal health, which is the mechanism that produces the network's most pronounced geographic inequity. A family in a county with a stable tax base may find robust services. A family in a rural county with a declining population and a constrained budget may find the same service categories listed on a website with a waitlist attached and no clear timeline.

More than one in ten AAAs report drawing on agency reserves to cover funding gaps for nutrition, case management, and long-term care assessments, per the 2025 National AAA Survey. Among agencies with waitlists, the longest backlogs are in precisely the services that keep people out of nursing homes: home-delivered meals, personal care, and homemaker and chore services. The irony is sharp and not abstract. The services most effective at preventing expensive institutional placement are the ones most likely to be rationed when budgets contract.

Families engaging with the AAA network need to know this before the first call, not as a reason to skip the call, but as a planning frame. A service that exists on paper may have a waitlist in practice. Asking about timelines on first contact, as a planning question rather than a challenge, gives a family the information it needs to decide what else it must pursue in parallel.

The Demographic Pressure Coming Into Full View

Americans 65 and older are projected to grow from 58 million in 2022 to 82 million by 2050, a 42% increase. By 2030, more than 20% of the U.S. population will be over 65. Alzheimer's prevalence could more than double by 2050, from 6 million to 13 million, and Alzheimer's generates among the most intensive caregiving demands across the disease spectrum. It is also explicitly covered by NFCSP eligibility, which means the program designed to support caregivers is headed directly into the demographic current.

The household context amplifies the pressure in ways that policy discussions underweight. Over one-fourth of women ages 65 to 74 lived alone in 2023; among women 85 and older, that share reaches 50%. These are individuals who will need community-based support rather than family in the same household, because there is no family in the same household. The assumption that informal family care will absorb this demand is unsupported by the data. It is an assumption built on a household structure that is already eroding.

The older population is also becoming more racially and ethnically diverse, with the non-Hispanic white share projected to drop from roughly 75% to 60% by 2050. AAAs are being asked to serve communities with historically less access to formal aging services, often across language, cultural, and trust barriers that take sustained institutional investment to address. That investment is not currently funded at the scale the demographic shift requires.

The average caregiver for an older adult is 49 years old, still employed, often still raising children. Caregiving does not happen in cleared space. It happens in the margins of a life that is already full, and that is exactly the condition under which external support has the highest marginal value.

OAA Reauthorization: Where It Stands and Why It Matters

The Older Americans Act was last reauthorized through fiscal year 2024. Since then, the programs it authorizes have operated on continuing resolutions: no new funding commitments, no program expansions, no structural updates to a law whose oldest provisions were written for a different demographic reality. A bipartisan reauthorization bill passed the Senate in 2024. It was stripped from a must-pass spending package in December 2024 at the last minute and has not been signed into law.

That is not a technical setback. It is a policy failure with direct service consequences, and the failure landed at the worst possible moment in the demographic curve.

What the stalled bill would have done is material. It would have increased authorized funding from approximately $2.3 billion to $2.76 billion in fiscal year 2025, roughly a 20% increase. It would have expanded caregiver supports and direct care worker provisions. It would have added home modification and weatherization support for older adults. Each of those provisions addresses a documented gap in the current system, a gap that is widening as the 65-and-older population accelerates toward 82 million.

The cost-offset argument deserves direct statement because it is routinely underweighted in reauthorization debates. AAA services demonstrably delay or prevent Medicaid-funded nursing home placement. Medicaid is the primary payer for long-term institutional care in the United States, and nursing home placement is among the most expensive items in that budget. The OAA network functions, among other things, as a cost-containment mechanism for a program that would otherwise face far greater strain. Defunding or stalling the network does not eliminate the cost; it shifts it downstream, where it is larger and harder to manage.

For families engaging with AAAs right now, the reauthorization status is practically relevant. What is funded at a local agency reflects what Congress has authorized and what federal formula grants have delivered. Asking a coordinator what services are currently available, what is on waitlists, and whether recent funding changes have affected capacity is a legitimate question, not an imposition.

Finding Your AAA and Making the Call Worth Making

The Eldercare Locator at eldercare.acl.gov is the federally maintained tool for finding a local AAA by zip code. It works, and the federal government maintains it reliably, which is not something you can say about every government-maintained database in this space. The call or visit that follows will typically connect a family with an information and referral specialist, or at many AAAs, a case manager who can assess needs and coordinate access to available services.

What to ask for specifically matters. AAA staff are responsive to direct requests, and the intake process can otherwise become a general conversation that does not surface specific programs. Ask for a needs assessment. Ask about caregiver support services under the National Family Caregiver Support Program by name, and ask about eligibility for the caregiver specifically, not only for the care recipient. Ask about long-term care consultation. Ask whether there are waitlists for in-home or meal services. That last question is pessimism to avoid — it is the question that lets a family plan rather than be surprised in six weeks.

Benefits counseling through AAAs can surface Medicaid home and community-based programs, Medicare Savings Programs, and other benefits a family may qualify for but has never enrolled in. Most families lack the time or the framework to understand which federal and state programs interact with their specific situation. A benefits counselor at an AAA has that framework and applies it without a billing clock running. That is a rarer resource than it should be.

The honest expectation to carry into first contact: availability varies by location, waitlists are real in many places, and the local AAA is a starting point rather than a complete solution. Knowing what exists, what the gaps are, and what the timelines look like gives a family the information it needs to make better decisions about what else it must pursue independently. That is not a limitation of the network. It is what informed engagement with any public system actually looks like.