Health Insurance Options for Full-Time Family Caregivers

Why Full-Time Caregivers Face a Distinct Health Insurance Problem There are roughly 63 million family caregivers in the United States. Most manage caregiving alongside paid…

Why Full-Time Caregivers Face a Distinct Health Insurance Problem

There are roughly 63 million family caregivers in the United States. Most manage caregiving alongside paid employment, so the insurance gap stays uncomfortable but containable. The problem sharpens for those who leave or reduce work entirely, because that decision severs the most common coverage mechanism available to working-age adults: employer-sponsored insurance.

The arithmetic is punishing. Professional in-home care averaged approximately $5,720 per month in 2024. Families who cannot sustain that cost turn to informal caregiving, which typically means one adult reducing or abandoning paid work. That same adult frequently carried the family's health coverage. The exit from employment is logical; what follows is not.

In 2025, 11.6% of working-age Americans between 18 and 64 lacked health insurance. Full-time family caregivers who exit the workforce sit squarely within that at-risk population, often without savings or severance to buy time while sorting through options that were never designed to work together. I think the more honest framing is that these options were not designed at all, at least not with the caregiver in mind. They accreted over decades, each program responding to a different political moment, each with its own income thresholds, eligibility triggers, and enrollment windows. The result is a landscape that rewards fluency in bureaucratic navigation, which is precisely the capacity someone providing intensive daily care has the least of.

This piece maps that landscape with a specific focus on the caregiver's own coverage, not the care recipient's, except in one meaningful category where the caregiving work itself comes with coverage attached.

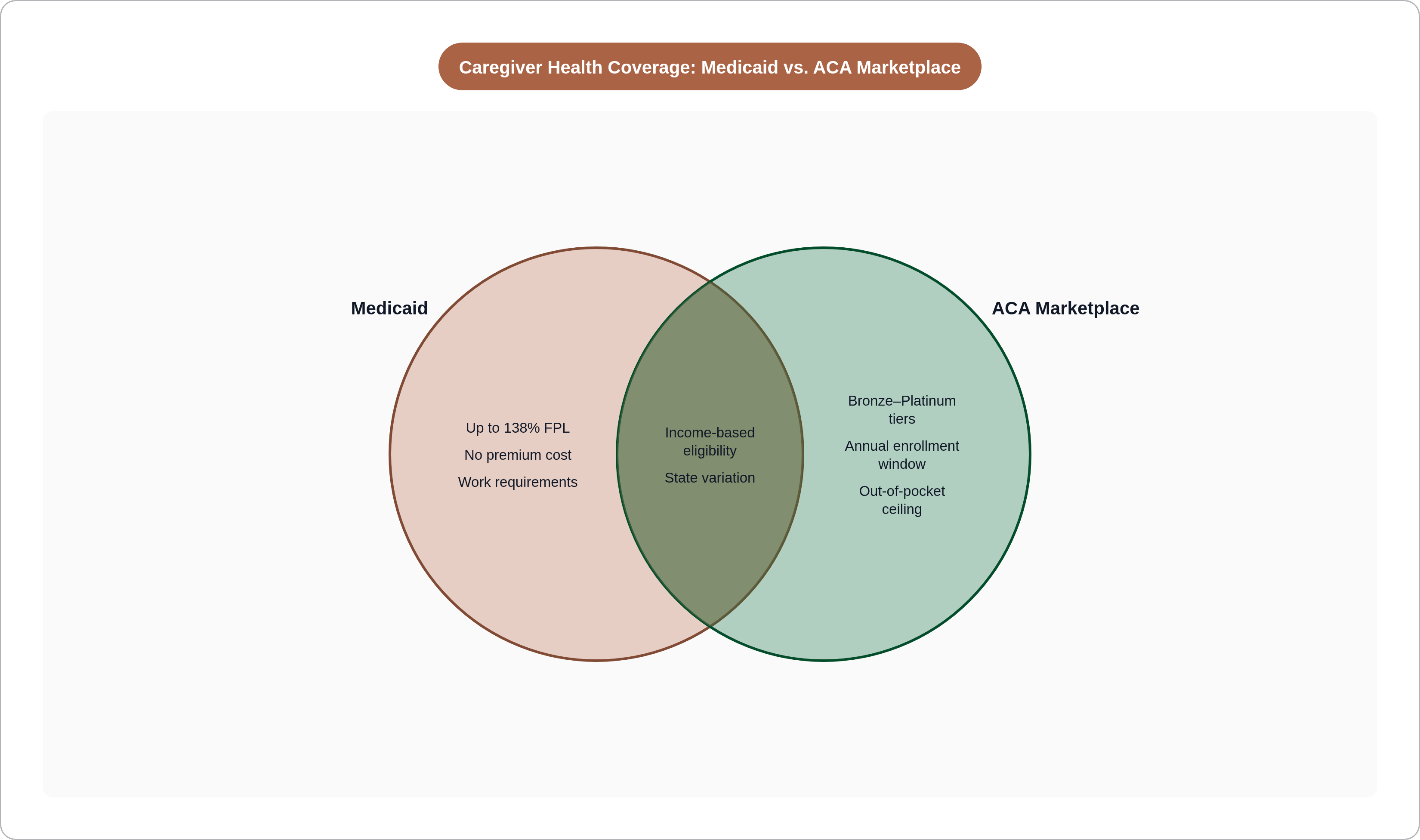

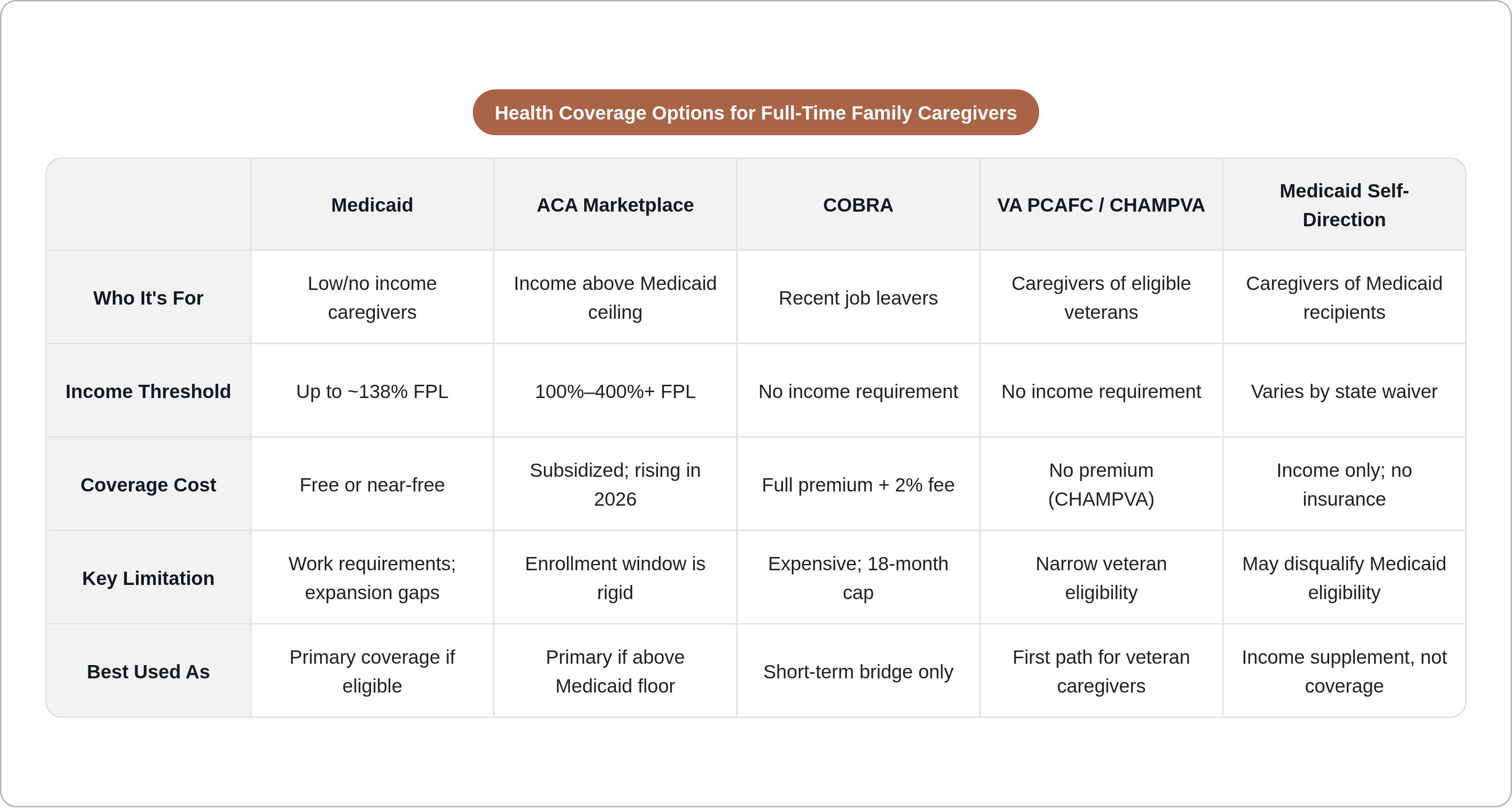

Medicaid as the First Stop for Caregivers with Low or No Income

When income drops substantially, Medicaid is the logical first door. The Affordable Care Act expanded eligibility to individuals earning up to 138% of the federal poverty level, approximately $21,597 for a single adult in 2025. Coverage is comprehensive and typically free or near-free: no premium, minimal cost-sharing. For a caregiver who has just left a salaried position, the financial relief relative to Marketplace alternatives is not marginal.

The AARP and National Alliance for Caregiving's 2025 Caregiving in the U.S. report found that 7.3 million caregivers between ages 18 and 64 already rely on Medicaid for their own coverage. The connection between caregiving and Medicaid enrollment is not theoretical; it is embedded in the data.

Two variables complicate the picture, one geographic and one legislative.

CDC data from 2025 found an uninsured rate of 9.0% in Medicaid expansion states compared to 18.1% in non-expansion states. A caregiver in Georgia and a caregiver in California with identical incomes may face entirely different coverage realities. State of residence is not a footnote in this analysis; it is often the determinative variable.

The second complication is the 2025 One Big Beautiful Bill Act, which introduced work requirements for certain Medicaid beneficiaries. Some enrollees must now document at least 80 hours per month of work, training, or qualifying activity to maintain coverage. Two exemptions are relevant: parents and guardians caring for dependent children, and individuals caring for people with disabilities. Those exemptions sound broader than they are. The definition of "caring for a person with a disability" remains inconsistently implemented across states, and caregivers who fall outside either exemption category face real uncertainty. But what if the care recipient's condition shifts, or a child ages out of dependency? The exemption's applicability is not self-executing.

KFF projects the OBBBA will reduce federal Medicaid spending by $911 billion over the next decade. Caregivers relying on Medicaid should verify their specific state's implementation of the new requirements rather than assuming federal exemptions translate cleanly into local coverage security. That gap between federal promise and state execution is where people actually lose coverage.

ACA Marketplace Plans and What Subsidies Are Actually Available in 2026

For caregivers whose income exceeds the Medicaid threshold, the ACA Marketplace is the next option. Premium tax credits require household income of at least 100% of the federal poverty level, approximately $15,650 for a single adult and $32,150 for a family of four in 2026. The range between that floor and the Medicaid ceiling is where subsidized Marketplace coverage can make financial sense, provided the caregiver can absorb even a reduced premium.

The 2026 environment is materially more expensive than recent years. The enhanced subsidies that had substantially reduced premiums since 2021 were not renewed. For a caregiver managing competing household expenses on reduced income, this is not an abstraction.

Enrollment timing now carries more consequence than it once did. Open enrollment runs November 1 through January 15 in most states. The OBBBA eliminated year-round enrollment based on income fluctuations, a pathway that had specifically served caregivers whose financial circumstances shift mid-year. Plans are no longer automatically renewed; caregivers must actively reenroll and update income, household composition, and other details annually. Missing the window is not a bureaucratic inconvenience; it means going uninsured until the following November.

Plan architecture deserves attention before choosing. Bronze plans carry the lowest premiums and the highest cost-sharing; Silver, Gold, and Platinum plans trade higher premiums for lower out-of-pocket exposure. Cost-sharing reductions, which lower deductibles and copays, are available only on Silver plans for enrollees earning below 250% of the federal poverty level. For a caregiver with modest income who anticipates needing care themselves, a Silver plan with cost-sharing reductions often delivers more value than its premium suggests. It is also worth considering the out-of-pocket ceiling before selecting a tier: in 2025, that ceiling was $9,200 for an individual and $18,400 for a family. For someone managing reduced income alongside their own health needs, that ceiling is not a theoretical maximum.

COBRA and a Family Member's Plan as Short-Term Bridges After Job Loss

COBRA allows a former employee to continue employer-sponsored group coverage after leaving a job. Same plan, same network; the individual now pays the full premium plus a 2% administrative fee. That number tends to arrive as a genuine shock to someone who only ever saw their employee share deducted from a paycheck. COBRA applies to employers with 20 or more employees, and most states have mini-COBRA laws extending comparable rights to workers at smaller firms, though the specifics vary.

Duration is limited to 18 months. Cost is the central liability. For someone who has stopped earning income to provide care, sustaining COBRA premiums for 18 months is rarely realistic. COBRA is a bridge, and it is an expensive one.

The more useful option, when it exists: if a spouse or domestic partner has employer-sponsored coverage, losing a job constitutes a qualifying life event that opens a 60-day special enrollment window to join that plan. Group coverage through an employer almost always costs less than COBRA for comparable protection. That window closes on its own schedule, regardless of how much else is in motion. Missing it forces a return to COBRA or an uninsured gap, neither of which is where anyone wants to land.

COBRA's legitimate function is continuity during the weeks it takes to assess Medicaid eligibility, locate a spouse's plan, or orient toward Marketplace open enrollment. It should not be confused with a solution.

VA PCAFC: The One Program Where Caregiving Itself Comes With Health Coverage Attached

The VA Program of Comprehensive Assistance for Family Caregivers, PCAFC, is notable because it is the only major government program that explicitly pairs caregiver compensation with health coverage. For caregivers of eligible post-9/11 veterans, and under the expanded program some veterans from earlier eras, the benefits package includes a monthly stipend paid directly to the caregiver, access to CHAMPVA health insurance if the caregiver lacks other coverage, and mental health counseling.

CHAMPVA covers inpatient and outpatient care, mental health services, and prescriptions, with no premium for the caregiver. For a family caregiver who has left employment to care for a veteran and has no other coverage source, that combination of stipend and insurance is among the most comprehensive arrangements available to any caregiver in the United States. The contrast with every other program in this landscape is not subtle.

A recent VA final rule extended the transition period for legacy PCAFC participants through September 30, 2028. Eligible participants will not face stipend reductions from reassessment during that window, a degree of financial stability that is otherwise rare in caregiver benefit programs.

The application requires documentation and has specific eligibility criteria. That is not a reason to delay; it is a reason to treat PCAFC as the first path investigated rather than a fallback. VA benefits navigators and accredited claims agents exist to move applications through the process.

PCAFC is also the clearest evidence in domestic policy that a different model is possible, one that treats caregiving as compensable labor with legitimate occupational health needs. One might argue that this model could be extended beyond the veterans context — and it would not be a radical argument. Whether federal policy has the appetite to extend it is a different question, and the answer, observed over several decades, has been no.

Medicaid Self-Direction Programs That Pay Caregivers, and What Coverage They Do or Don't Include

Every state and the District of Columbia operates at least one Medicaid program allowing care recipients to direct their own care, including the option to hire a family member as a paid caregiver. These arrangements go by various names: Consumer-Directed Personal Assistance, Cash and Counseling, Self-Directed Services. The common thread is that Medicaid funds flow to the care recipient, who directs payment to the caregiver.

The care recipient must be Medicaid-eligible and require assistance with activities of daily living. The caregiver typically must meet state-specific training or certification requirements. Pay rates generally track home care aide wages in the state, roughly $13 to $18 per hour or more depending on geography. For a caregiver who was previously providing the same labor for nothing, this represents a meaningful economic shift.

The coverage implication cuts both ways — and this is where caregivers are often caught off guard. Income from self-direction counts as earned income for eligibility purposes. A caregiver who was previously income-eligible for Medicaid may find that self-direction wages push them above the threshold, requiring a pivot to Marketplace coverage. That raises an important question: have you run the full household income calculation before assuming this income is an unambiguous improvement? Medicaid eligibility is calculated on total household income, and self-direction wages are treated no differently than wages from any other employer.

What self-direction programs do not include is health insurance for the caregiver. The income is the benefit. Coverage remains the caregiver's responsibility to source independently.

AARP's Public Policy Institute estimates that the aggregate value of unpaid family caregiving exceeds $1 trillion annually. Total Medicaid spending reached approximately $931.7 billion in 2024. Self-direction programs represent a partial acknowledgment of caregiving's economic value; the fraction of that value they actually compensate remains small. Waiting lists affect many waiver-based self-direction programs, while state plan programs are entitlements without waiting lists but with narrower scope, further constraining who actually benefits.

CHIP and Other Coverage for Caregiver Households With Children

CHIP, the Children's Health Insurance Program, provides coverage to children in households earning too much for Medicaid but too little to afford private insurance. Income limits vary by state but generally extend well into middle-class income ranges.

CHIP does not cover the caregiver. Its relevance is indirect but real: securing children's coverage through CHIP frees household budget that a caregiver-parent might otherwise direct toward a more expensive family plan on the Marketplace. Covering children separately through CHIP can make a lower-cost individual plan viable for the adult.

CHIP enrollment is also open year-round, unlike Marketplace plans with their annual windows. For a family that becomes a caregiving household mid-year, that distinction is worth knowing before the next November.

What Medicare Covers, and Doesn't, for Working-Age Caregivers

Medicare is not available to most working-age adults. Unless a caregiver has a qualifying disability, End-Stage Renal Disease, or ALS, Medicare is not a personal coverage option before age 65. For the population this piece addresses, Medicare is largely irrelevant as a coverage mechanism for the caregiver.

Why exactly does this matter? Because persistent confusion about its role leads to real miscalculation. KFF has found that four in ten adults incorrectly believe Medicare, rather than Medicaid, is the primary payer for home care and nursing services for low-income people. Medicaid covers nearly two-thirds of all home care spending in the United States, per KFF data from 2023, while Medicare's home care benefit is far narrower and time-limited. A caregiver who misunderstands this distinction may miscalculate both the care recipient's coverage and their own financial planning.

Two recent developments are worth noting, though neither constitutes health insurance for caregivers. Original Medicare began covering caregiver training in 2025, a policy recognition of caregivers' role rather than a direct benefit. The GUIDE model, launched in July 2024 for caregivers of people with dementia, provides 24/7 support lines, care coordination, and respite services. These are support benefits, not coverage. They belong in a different column of any honest accounting of what this system actually provides to caregivers.

How to Choose Among the Options Based on Your Actual Situation

The honest answer is that there is no universal correct path, and anyone who tells you otherwise is selling a simplification.

What income the caregiver's household actually earns, and from what sources including any Medicaid self-direction wages, is the variable that determines where the analysis begins. Income below approximately 138% of the federal poverty level points toward Medicaid, with an immediate check of state expansion status. Non-expansion states require a different analysis, and the gap between states is wide enough to be determinative.

Income above the Medicaid ceiling, with no employer or spouse's plan available, points toward the Marketplace. In 2026, that means accepting a more expensive environment and treating the open enrollment window as a hard deadline, not a soft one.

A caregiver who has just left a job should immediately clock the 60-day window to join a spouse's employer plan if one exists. COBRA covers the days and weeks it takes to assess longer-term options; its cost makes it unsuitable beyond that transitional function.

Caring for a veteran changes the analysis substantially. PCAFC and CHAMPVA should be investigated first. Nothing else in this landscape offers a comparable combination of stipend and no-premium coverage for the caregiver, and treating it as a fallback wastes time the caregiver does not have.

Self-direction wages require factoring into eligibility calculations for both Medicaid and Marketplace before accepting that income stream. The numbers sometimes point in counterintuitive directions.

The variables that shift the answer include state of residence, household size, age, the veteran status of the care recipient, and whether any household member retains employer coverage. Benefit discovery tools and enrollment assistance programs exist because navigating Medicaid rules, Marketplace timelines, VA applications, and self-direction income calculations simultaneously is not a reasonable expectation for someone also providing intensive daily care. Using those resources is not a workaround. It is the appropriate response to a system assembled without the caregiver in mind, and that fact alone deserves more scrutiny than it typically receives.