Medicaid Programs That Pay Family Caregivers

Why so many family caregivers go uncompensated despite doing essential work The numbers are hard to sit with. AARP's Caregiving in the U.S. 2025 report counted approximately 63…

Why so many family caregivers go uncompensated despite doing essential work

The numbers are hard to sit with. AARP's Caregiving in the U.S. 2025 report counted approximately 63 million American adults providing ongoing care to someone with a medical condition or disability, nearly one quarter of all U.S. adults. These are not people occasionally driving a parent to an appointment. Many have restructured their working lives entirely. KFF focus groups have documented caregivers reducing hours or leaving jobs outright. On average, they spend roughly $7,242 per year, about 26% of their income, out of pocket on caregiving expenses, and approximately half have experienced measurable financial setbacks.

AARP's Valuing the Invaluable 2026 report put the total economic value of adult caregiving in 2024 at $1.01 trillion, a figure that exceeds total Medicaid spending that year. What that number reveals is structural: the formal care economy is built on labor it does not pay.

The compensation gap did not happen by accident. Courts and legislatures long treated family care as an extension of familial obligation rather than a compensable service. That legal and cultural baseline proved remarkably durable, even as care itself grew more medically intensive and more expensive to replace. The default was unpaid care, and defaults are hard to dislodge.

So the more useful question becomes a narrower one: for caregivers who do qualify for compensation through existing public programs, why is access so inconsistent, and what does the landscape actually look like?

How Medicaid became the primary funder of home-based long-term care

Medicaid did not set out to become the country's dominant long-term care payer. It became one somewhat reluctantly, as nursing facility costs ballooned into one of its largest expenditure categories and advocates pressed for care to move out of institutions. By 2023, Medicaid paid for roughly two-thirds of all home care spending in the United States, per KFF. Over one-third of all Medicaid spending now flows to long-term care, with the majority directed toward home and community-based services rather than nursing facilities.

The shift is both a policy choice and a financial calculation. Home-based care is, in most cases, less expensive than nursing facility placement, and it aligns with what most care recipients actually want. An estimated 5.1 million Medicaid enrollees currently use home care for help with daily activities. Separately, roughly 8 million family caregivers rely on Medicaid as their own health insurance, meaning their stakes in these programs run in two directions: they are both the labor supply that makes home care viable and a population dependent on Medicaid for their own coverage.

Nearly all of Medicaid's home care funding flows through optional services that states choose to offer. Federal law establishes the framework; states decide how much to build inside it. That architecture explains, more than anything else, why outcomes for caregivers vary so dramatically across state lines.

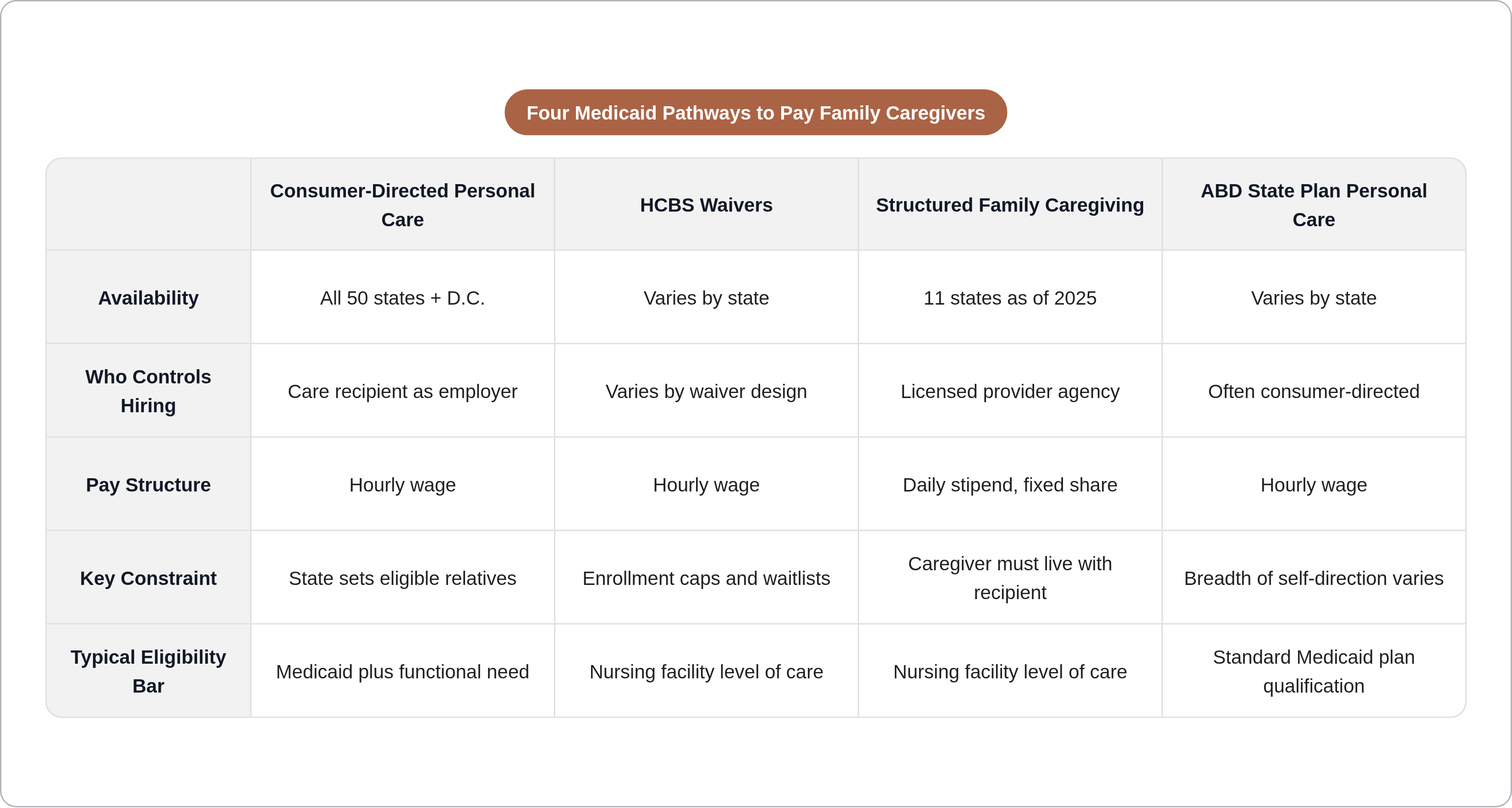

The four main program structures through which Medicaid pays family caregivers

Four distinct mechanisms allow Medicaid to put money in a family caregiver's hands. Which pathway applies to a given family depends on the state, the care recipient's diagnosis and level of need, and the caregiver's relationship to them.

Consumer-directed personal care is the dominant model. Available in some form in all 50 states and the District of Columbia, it gives the Medicaid recipient authority to select, train, and pay a caregiver of their choosing — often a family member. The recipient functions, in effect, as the employer.

Home and community-based services waivers, authorized under several federal provisions (most commonly section 1915(c), 1915(i), 1915(j), and 1915(k)), allow states to fund home care services not covered under standard Medicaid rules. Most HCBS waivers require the care recipient to meet nursing facility level of care. Waivers may also carry enrollment caps and waiting lists; qualifying does not guarantee immediate access.

Structured Family Caregiving delivers a daily stipend through a provider agency rather than an hourly wage. The agency supervises the caregiver and passes a portion of the per diem directly to the family member. As of 2025, it is available in eleven states.

Aged, Blind, and Disabled Medicaid state plan personal care serves beneficiaries who qualify through their state's standard Medicaid plan rather than a waiver, often with a consumer-directed option, though the breadth of that option varies considerably.

Not all four structures are available everywhere. This is precisely why general advice about "Medicaid paying family caregivers" so often fails to translate into anything actionable.

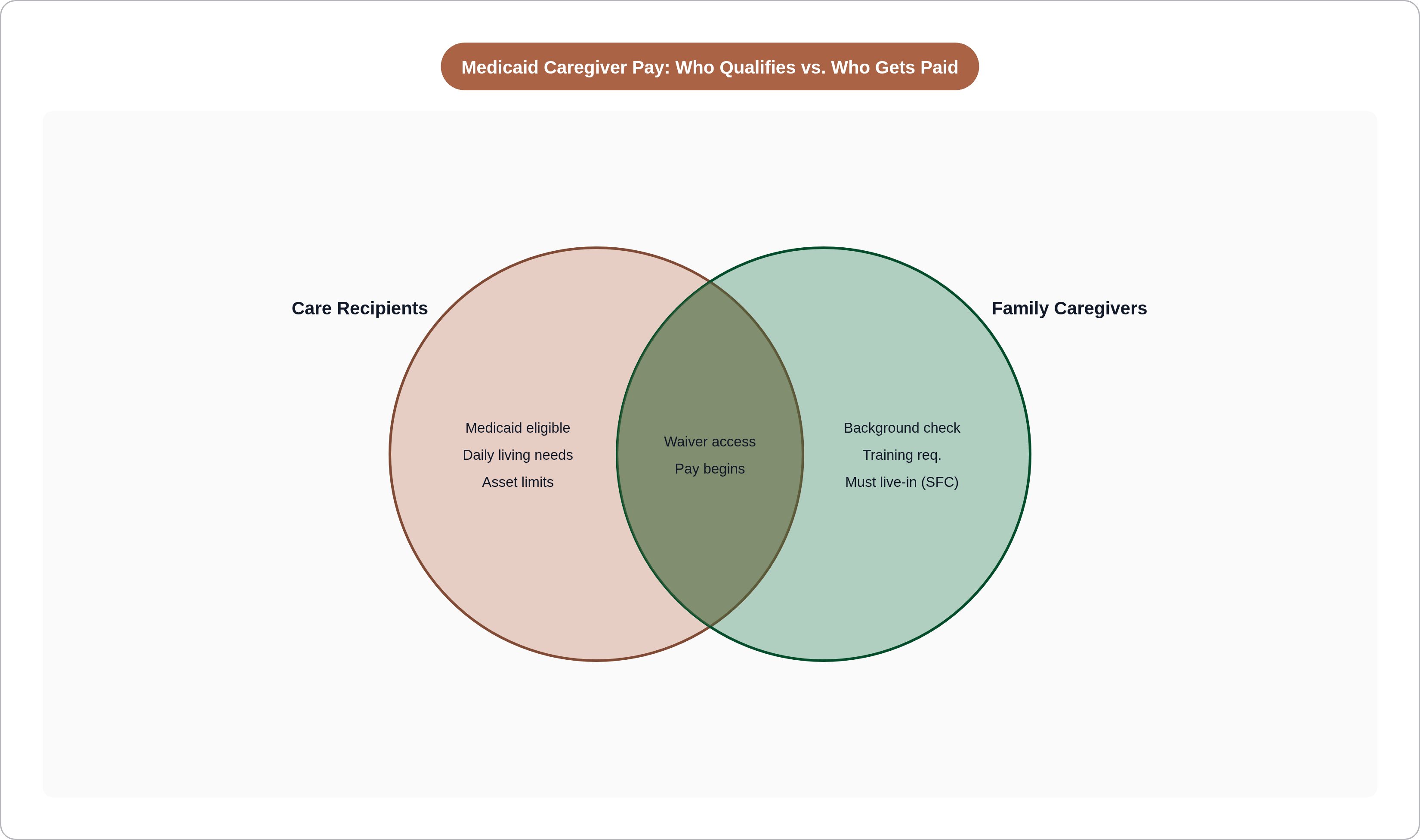

Who qualifies, on both sides of the caregiving relationship

Eligibility runs in two directions at once: the care recipient must qualify for Medicaid and demonstrate sufficient need, and the caregiver must satisfy a separate set of state-defined requirements.

For care recipients, Medicaid eligibility is the floor. For HCBS waivers, income and asset thresholds apply: 2026 general thresholds run to approximately $2,982 per month in income and $2,000 in countable assets. Beyond financial eligibility, the recipient must demonstrate a need for assistance with activities of daily living. Waiver programs typically require nursing facility level of care, a bar that reflects genuine functional limitation rather than bureaucratic convention.

Caregivers, for their part, are routinely required to pass background checks and complete some form of training or certification before compensated care can begin. The specifics differ enough by state and program that no universal preparation applies.

The spouse question deserves its own attention. For most of Medicaid's history, spouses were excluded from paid caregiver roles on the theory that spousal care was a marital obligation. Per KFF's 2025 survey, 44 states now allow waivers to pay legally responsible relatives, a category that typically includes spouses, and more than 30 states explicitly permit spousal payment under at least some programs. That is a meaningful shift from a not-distant historical baseline, and it remains underappreciated by most families encountering these systems for the first time.

Adult children are the most common paid family caregivers. Parents of minor children are generally excluded. And in high-demand states, qualifying for a waiver program and actually accessing it can be separated by months or years.

What Structured Family Caregiving pays and how the stipend model works

Families regularly misunderstand Structured Family Caregiving. Under this model, Medicaid reimburses a licensed provider agency a daily rate. The agency conducts regular home visits, maintains supervisory oversight, and is required to pass a fixed minimum share of that per diem directly to the caregiver.

State rates illustrate the range. South Dakota's SFC rates, effective July 1, 2026, run from $82.00 per day at base level to $102.52 at tier one and $114.81 at tier two, with a minimum of 50% required to flow to the caregiver. Missouri's rate is $103.80 per day, with at least 65% directed to the caregiver. Across programs, typical caregiver payments run roughly $40 to $70 per day, adjusted for acuity. As of 2025, SFC is operational in eleven states: Connecticut, Georgia, Indiana, Louisiana, Massachusetts, Missouri, Nevada, North Carolina, Ohio, Rhode Island, and South Dakota. North Dakota offers a functionally comparable model under a different program name.

Two structural features define SFC and determine whether it fits a given family. The caregiver must live with the care recipient, which immediately narrows the eligible pool relative to hourly models. And the per diem structure means pay does not scale with hours. For a caregiver providing continuous supervision to someone with advanced dementia or significant physical dependence, this can be an advantage: compensation is consistent regardless of a given day's intensity. For someone providing a few hours of assistance to a more independent recipient, an hourly model may be more efficient. These distinctions matter when a family is deciding whether enrollment is worth pursuing.

How pay rates are set and what caregivers in different states actually earn

Per KFF, family caregivers and personal care providers receiving Medicaid compensation earn approximately $18 per hour on average. That average conceals variation wide enough to produce materially different lives. California and New York pay informal caregivers up to $20 per hour. Mississippi and Alabama range from $11 to $13 per hour. The Bureau of Labor Statistics reported that home health and personal care aides earned nearly $17 per hour in 2024, a figure many states reference when setting caregiver compensation.

Several factors drive the variation. Cost of living matters but does not fully explain it. Whether care flows through an agency or directly affects the administrative overhead extracted from the rate. The specific waiver or state plan authority in use carries different rate-setting flexibility. Acuity level and caregiver training or certification can further adjust what a state pays.

California's In-Home Supportive Services program illustrates how rates can be structured at scale. IHSS sets wages county by county through collective bargaining, with a statewide floor of $16.50 per hour effective January 1, 2025, adjusted by CPI to approximately $16.90 per hour effective January 1, 2026. Counties with stronger negotiating positions pay more.

The practical implication is straightforward: a caregiver in a high-cost state with a well-funded waiver can earn meaningfully more than one in a state with a thinner program. Understanding what is available locally is the determinative step, not a supplemental one.

California's IHSS and New York's CDPAP as the two largest programs in the country

California's In-Home Supportive Services and New York's Consumer Directed Personal Assistance Program appear constantly in discussions of paid family caregiving, and there are real reasons for that. Both demonstrate what happens when a state fully commits to self-direction at scale. Neither is easily transplanted elsewhere, and reading them as representative of what most states offer would be a significant misreading.

California's IHSS is the largest paid family caregiver program in the country by almost any measure. Approximately 771,650 recipients are projected for fiscal year 2025-26, supported by roughly $28.5 billion in total funding, of which about $10.6 billion comes from the state's General Fund. IHSS is notably permissive in who it allows as a paid caregiver: siblings, adult children, nieces, nephews, friends, and spouses are all eligible. That permissiveness matters because many states still restrict spousal participation entirely or conditionally.

New York's CDPAP allows Medicaid members to hire friends or family as personal caregivers with real flexibility, though it excludes the member's spouse, their designated representative, and parents of CDPAP consumers under 21. The program underwent substantial structural change recently. Through 2024, more than 600 fiscal intermediaries administered it across the state. On April 1, 2025, following 2024 state budget legislation, it consolidated under a single statewide fiscal intermediary. The change simplified administration but created significant transition friction for families already mid-enrollment — a disruption greater than Albany anticipated.

Both programs are worth understanding. Neither offers much direct guidance to a caregiver in Arkansas or Iowa.

Why the same federal framework produces such different outcomes state to state

The federal Medicaid statute establishes what states may do with respect to home and community-based care; it does not mandate most of it. HCBS services and the vast majority of paid family caregiver programs are optional. States choose whether to offer them, which populations to serve, what rates to set, and whether to allow family members, including spouses, to be hired. The federal government defines the permissible structures. States decide how much to build inside them, or whether to build at all.

Per KFF's 2025 survey, all responding states allow self-direction under at least some circumstances and pay family caregivers under some circumstances. "Some circumstances," though, spans from a narrow pilot serving a few hundred people to a statewide program serving hundreds of thousands. That every state technically allows self-direction is true. It is also practically misleading if read as implying anything like uniform access.

Payments to family caregivers are most common in waivers designed for people with intellectual or developmental disabilities. Families caring for elderly relatives or those with physical disabilities may find substantially fewer options in their state, within the same federal framework. Forty-one states allow enrollees to set payment rates for their caregivers; 39 allow enrollees to determine how Medicaid funds are allocated across services. States that do not offer these controls provide a meaningfully more constrained self-direction experience, even if a program technically exists.

Two families in neighboring states with identical care situations can face radically different programs, pay rates, and caregiver eligibility rules. The federal framework sets the boundaries. What states have built inside those boundaries varies enormously, and some states have not built much.

How to find out which programs are available in your state and how to apply

The complexity is genuine. Eligibility rules, program names, administrative structures, and application processes differ enough by state that families regularly fail to access programs they qualify for — not from lack of diligence, but because the information is genuinely fragmented. I have watched families spend months pursuing the wrong program because the right one had a different name in their state, or because no one told them the waiting list had closed two years earlier.

Several starting points cut through that fragmentation reliably. State Medicaid agency websites are the authoritative source for what programs exist and under what authority. Medicaid.gov's HCBS waiver finder allows users to identify which waiver programs are active in a given state and what populations they serve. State-specific Aging and Disability Resource Centers, federally funded to help people navigate long-term care options, can translate program structures into plain language for individual families.

When contacting a state program, four questions are worth asking explicitly: Does this program allow family members to be paid caregivers? Does it permit spousal payment? Is there a waiting list, and if so, how long? What training or certification must a caregiver complete before compensation begins? The answers define whether a given program is actually accessible to a specific family.

One procedural reality that consistently catches families off guard: in self-directed programs, Medicaid eligibility runs through the person receiving care, not the caregiver. The care recipient initiates enrollment. A family member researching compensation options is, in effect, beginning an application process on behalf of their relative. Misunderstanding that sequencing is a common and costly source of delay.

Fiscal intermediaries and financial management services organizations exist specifically to help self-directing participants handle payroll, taxes, and compliance. Families are not expected to become tax administrators. Knowing these intermediaries exist, and asking the state program how to connect with them, removes a barrier that stops many people before they start.

The gap between programs that exist and families who access them is mostly an information problem — frustrating, but specific enough to be worth addressing.